Real Estate Insights & Community News

jen's market in a minute - broadneck updates for july 2022

jen’s market in a minute this week is focusing on the broadneck peninsula and what the latest real estate trends are showing us for the 21012 and 21409! is the market really crashing? the bubble bursting? jen breaks down all the data to give an expert look into our local market.🧐🤓 if you have ques

Read More

Two Reasons Why Today’s Housing Market Isn’t a Bubble

Two Reasons Why Today’s Housing Market Isn’t a Bubble You may be reading headlines and hearing talk about a potential housing bubble or a crash, but it’s important to understand that the data and expert opinions tell a different story. A recent survey from Pulsenomics asked over one hundred housing

Read More

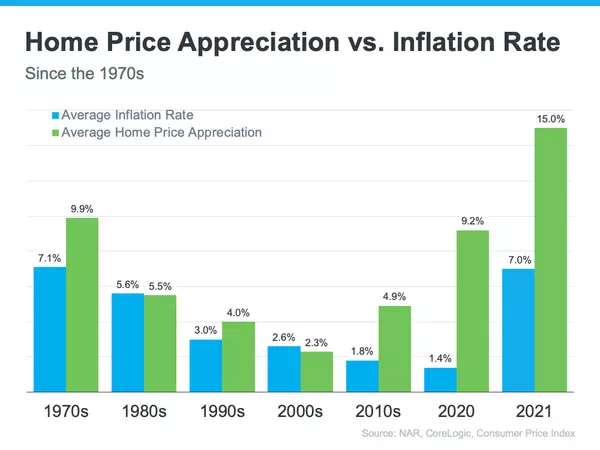

Homeownership Is a Great Hedge Against the Impact of Rising Inflation

Homeownership Is a Great Hedge Against the Impact of Rising Inflation If you’re following along with the news today, you’ve heard about rising inflation. Today, inflation is at a 40-year high. According to the National Association of Home Builders (NAHB): “Consumer prices accelerated again in May as

Read More

Categories

Recent Posts