Real Estate Insights & Community News

Fewer Homes Are Selling Above Their List Price

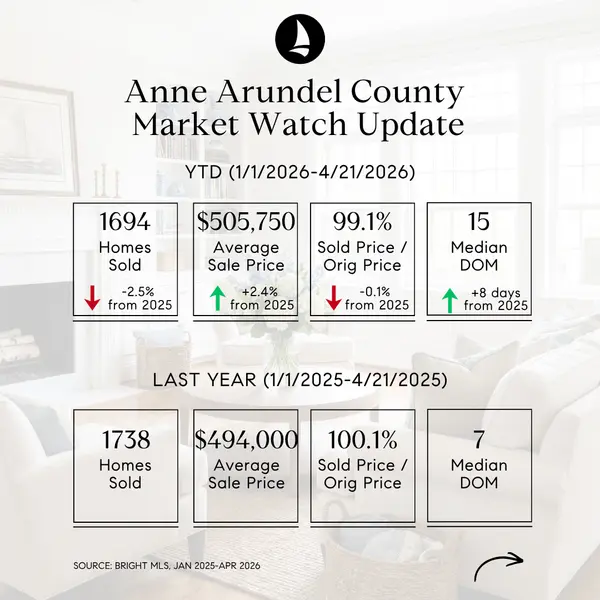

Anne Arundel County Real Estate Market Update Anne Arundel County Real Estate Market Update 2026: Why More Homes Are Selling Below Original List Price The market has not stopped. It has normalized. That shift is creating more opportunity for buyers, while making pricing strategy more important tha

Read More

Spring 2026 Real Estate Roadmap: Free Guides for Buyers and Sellers

Spring 2026 Edition Buying or Selling a Home This Spring? Start with Our Free Spring 2026 eGuides Spring is one of the busiest real estate seasons of the year, and this one comes with more choices, more strategy, and more questions for both buyers and sellers. To help you move with confidence in Gre

Read More

Unlock Savings with Maryland’s Homestead Tax Credit (Homestead Exemption): Your 2026 Guide

Unlock Savings with Maryland’s Homestead Tax Credit If you own a home in Maryland, there is a simple, one-time step that can help protect you from big jumps in your property taxes over time: applying for the Maryland Homestead Tax Credit (often called the Homestead Exemption). Many homeowners assume

Read More

Categories

Recent Posts